|

||

Trust setup refers to the transfer of an individual's or group's assets to a trust while still retaining the right of management, utilization and allocation. The individual /group maintain the right to determine how the funds are allocated and / or utilized, facilitating successful wealth transfer between generations. |

||

|

||

|

||

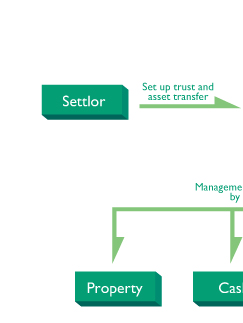

A settlor is the owner of the asset. In law a settlor is a person who settles assets in trust for use by named beneficiaries. The settlor may also be the trustee. |

||

|

||

Trustee is a legal term that refers to a holder of property/assets on behalf of a beneficiary. A trustee is usually a bank or trust company. The trustee manages the trust according to the objectives and targets set by the settlor. |

||

|

||

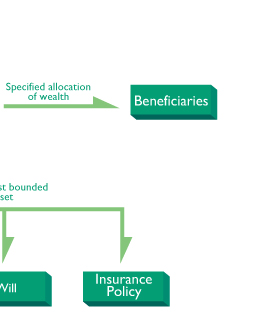

A trust can be set up either to benefit particular individuals, or for a particular purpose; typical examples are a Will Trust for the testator's children and family; Spendthrift Protection to ensure a life long income; or a Charitable Trust. In all cases, the trustee may be a person or company, whether or not they are a prospective beneficiary. Once a trust has been created and a trustee decided on, the trustees are the legal owners of the trust property and they are obliged to hold the property for the benefit of one or more individuals or organizations specified by the settlor, until the contract term expires or the objective of the trust is served. |

||

|

||

|

||

|

||

|

||

|

||

|

||

|

||

|

||

|

||

|

||

The purposes of setting up a trust fund are wealth protection, ensuring utilization based on the settlors intention and simplified inheritance procedure. But bear in mind that a trust fund is affected by the respective tax policy, inheritance legislation, jurisdiction system and political stability of the trust funds location. |

||

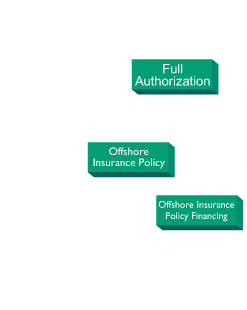

an insurance policy or future proceeds from the policy are included in the trust. This allows for beneficiaries to be provided for and the confidentiality of the insurance policy to be maintained. LIT are the ideal way to secure such goals as provision of financial security for dependents, education needs and venture capital.

an insurance policy or future proceeds from the policy are included in the trust. This allows for beneficiaries to be provided for and the confidentiality of the insurance policy to be maintained. LIT are the ideal way to secure such goals as provision of financial security for dependents, education needs and venture capital. the settlor transfers assets into the fund by installments or by a single payment. The trustee invests the assets in low risk financial products such as deposits, unit trusts, bonds and stocks. The proceeds are paid to the settlor as required.

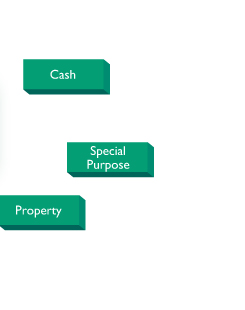

the settlor transfers assets into the fund by installments or by a single payment. The trustee invests the assets in low risk financial products such as deposits, unit trusts, bonds and stocks. The proceeds are paid to the settlor as required. Securities such as bonds and stocks are transfered to the trust fund. The trustee, usually a bank in this case, will manage and execute the trust. In this way the workload of wealth management by the beneficiary is kept to a minimum.

Securities such as bonds and stocks are transfered to the trust fund. The trustee, usually a bank in this case, will manage and execute the trust. In this way the workload of wealth management by the beneficiary is kept to a minimum. A professional trustee manages and develops the real estate in accordance with the trusts objective.

A professional trustee manages and develops the real estate in accordance with the trusts objective. a trust arrangement where both employer and employees contribute a fixed lump sum on a monthly basis, and an appointed trustee makes regular investments to increase the trust's value. Proceeds will be used for certain benefit programs for the employees.

a trust arrangement where both employer and employees contribute a fixed lump sum on a monthly basis, and an appointed trustee makes regular investments to increase the trust's value. Proceeds will be used for certain benefit programs for the employees. a trust setup to benefit named charitable organisations.

a trust setup to benefit named charitable organisations.